How to use it

Global ripple effects: Knock-on effects of EU, US, and China climate policies on developing countries’ trade

Published 07 January 2025

The world’s largest economies, the US, China, and the EU, are grappling with the impact of climate change, including how best to reduce emissions and mitigate its negative effects. The World Bank provides a report attempting to quantify the impact of new policies adopted by the three economies and how they are expected to affect developing countries.

Here’s how to use the report entitled Global Ripple Effects: Knock-on Effects of EU, US, and China Climate Policies on Developing Countries’ Trade.

Why is the report important?

As adverse effects of climate change become more apparent, governments are taking bolder steps to address carbon emissions and environmental degradation, including through trade and investment policies. While the US, China, and the EU may have the economic power to absorb negative costs and inefficiencies and reap the benefits of these policies, developing countries are likely to experience adverse effects from these policies in a way that could undermine the goals of reducing carbon emissions and environmental degradation. It is vitally important for all economies to understand what policies are adopted and their impact on economies and industrial sectors around the world so that developing countries can best leverage these policies. In addition, it is important for the three major economies to consider the negative effects of their policies to create the most appropriate and tailored policy design. This report highlights the policies and analyzes both the opportunities and challenges the policies present.

What’s in the report?

The report includes three key sections:

Introduction; Climate change mitigation policies in the EU, US, and China and their impacts on trade

- The EU, US, and China – together responsible for nearly half of global greenhouse gas (GHG) emissions – are taking different approaches to climate mitigation policy; the EU is focused on emissions pricing, the US on subsidizing clean production and clean technology adoption, and China on incentivizing efficiency improvements through its emissions trading system (ETS); these approaches have varying consequences on trade with producers and consumers in developing countries; this paper examines three main channels through which climate policies affect developing countries: shifts in supply and demand in trade sectors, price changes, and access to technology, and identifies sectors and countries most exposed to these policies. (pp. 2-3)

- The EU’s climate policy centers on the "Fit for 55" package, with the Critical Raw Materials Act for the Future of EU Supply Chains (CRMA) and the Corporate Sustainability Due Diligence Directive (CS3D) proposal, to revise and update EU climate, energy and transport legislation to achieve a 55 percent reduction in GHG emission by 2030; US federal climate policy is shaped by the Inflation Reduction Act (IRA) to address energy security and climate change mitigation through new federal spending and tax breaks to reduce carbon emissions; China focuses on low-carbon infrastructure, mineral sourcing through the Belt and Road Initiative (BRI), and emissions reductions through its ETS; the main differences between these policies is that they rely on carbon pricing, green subsidies, and regulations with different intensity; (p. 3)

- The use of carbon pricing and subsidies to support the green transition is warranted because of the presence of negative externalities; in developing countries with limited capacity, regulations can effectively reduce GHG emissions; varying uses of carbon taxes, subsidies, and regulations are expected to lead to differing impacts of climate policies on developing countries by reducing demand for carbon-intensive “brown” goods and increasing demand for low-carbon “green” goods; EU, US, and China climate policies share common impacts on trade, including restricting market access for sectors with high emission intensity, increasing demand for transition minerals while reducing demand for fossil fuels, and distorting competitive advantages through industrial subsidies for green technologies; positive effects of climate policies can be undermined when combined with discriminatory measures like domestic content requirements, which create distortions and lead to inefficient resource use. (pp. 4-5)

- Carbon pricing and preventing carbon leakage are climate policies impacting developing countries; since 2005, the EU’s ETS has placed a price on carbon and is the EU’s key tool for reducing emissions, featuring a system where around 10,000 covered companies must buy annual allowances under a cap which decreases over time to encourage companies to reduce emissions; "Fit for 50" ETS reforms include more ambitious emissions reduction targets and fewer allowances, expansion to cover maritime transport, and introduction of the CBAM carbon pricing system to reduce carbon leakage caused when industries relocate to jurisdictions with less stringent climate policies; China established the world’s largest ETS system in 2021 in terms of covered emissions - an intensity-based system with free but capped allowances allocated using benchmarks for each fuel and technology. (pp. 5-6)

- Impactful climate policies also include targets and incentives for energy efficiency, clean energy, and electromobility; the EU’s Renewable Energy Directive (RED) sets a binding target for the EU to obtain at least 42.5% of its energy from renewable sources by 2030, and its Energy Efficiency Directive (EED) mandates an 7% reduction in energy consumption by 2030; China’s 14th Five-Year Plan on Renewable Energy Development from 2021-25 targets a 50% increase in renewable generation and renewables accounting for 33% of electricity consumption. (pp. 6-7)

- The US IRA offers tax credits for companies and consumers, grants, and technical assistance to encourage clean energy production and consumption, with a requirement to source critical minerals and clean energy components from the US or US FTA partners; provisions expected to affect developing countries the most include clean energy tax credits, support for domestic clean energy manufacturing, incentives for EV adoption, and grants and loans to promote EV manufacturing; other EU and US regulations aim to lower emissions by setting carbon standards for new vehicles and encourage the transition to EVs while China has adopted new fuel efficiency standards to require vehicles to meet specific fuel consumption requirements; China also offers tax exemptions for EVs and plug-in hybrid EVs and fuel cell vehicles. (pp. 7-8)

- The US IRA’s local content requirements for clean energy manufacturing include that all steel and iron used must be made in the US, and that at least 40% of manufactured products and components used must be mined, produced, or manufactured in the US; for EVs, tax rebates and credits are eligible only if final assembly takes place in North America and a large percentage of components, including batteries, are sourced in North America or from US FTA partners, with requirements increasing over time. (p. 8)

- The EU introduced the Green Industrial Plan in 2023 to increase European competitiveness by simplifying regulations for developing net-zero industries like batteries and windmills); one initiative is the CRMA to boost the EU’s critical raw materials supply and diversify sourcing, recycling, and innovation; CRMA sets targets for sustainable supplies of critical raw materials (most important economically, vital for numerous industrial ecosystems, high supply risk) and strategic raw materials (materials expected to grow exponentially in supply but with complex production requirements and high risk of supply issues); CRMA is meant to correct the EU’s heavy reliance on a few supplier countries; unlike the US and EU, China sources a large share of its raw materials through investments abroad, particularly through the BRI. (pp. 8-10, Table 1, Figure 1)

- The EU also introduced the EU Deforestation Regulation (EUDR) to promote the consumption of deforestation-free products and lessen the EU’s impact on global deforestation, GHG emissions, and biodiversity loss; and the CS3D aimed at preventing environmental degradation and requiring large corporations to adopt sustainability and due diligence practices to address negative impacts on the environment and human rights; the CS3D went into force on July 25, 2024 but implementation of the EUDR has been delayed to the end of 2025. (pp. 10-11)

Implications of trade-related climate policies for developing countries

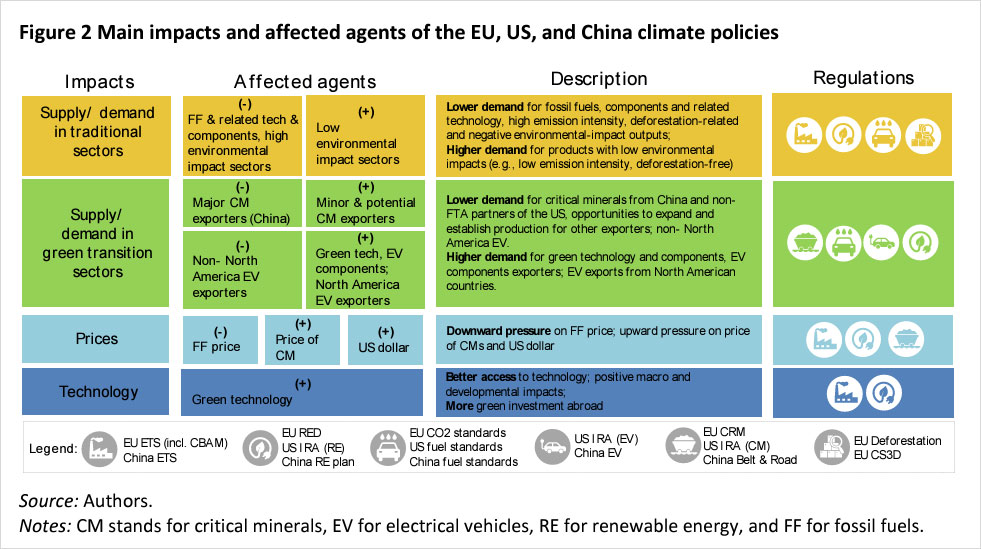

- EU, US, and Chinese climate policies will negatively affect trade in some sectors of developing countries and create positive opportunities in others; the magnitude and direction of impact depends on a country’s product coverage and its particular conditions; supply and demand analysis focuses on traditional sectors like fossil fuels and manufacturing and green transition sectors like EVs, batteries, and critical minerals, with demand for outputs in fossil fuels and environmentally damaging sectors declining and demand for green transition inputs increasing depending on the current dominance of the exporters; a country’s exposure can be measured through its sector exposure – how much a sector is focused on the market where the policy adjustment occurs – and its economic exposure – broader repercussions on a country’s economy measured by the share of the affected products’ exports to the destination market in relation to the country’s GDP. (p. 11-13, Figure 2)

- The EU’s ETS, EED, and RED, the US IRA, and China’s renewable targets and ETS are expected to significantly affect fossil fuels and related technologies by incentivizing the use and adoption of renewable energy and green technologies or rewarding increased fuel efficiency, thus reducing demand for fossil fuels; developing countries’ fossil fuels sectors have varied exposure to these policies; Libya, Azerbaijan and Angola are likely to experience significant economic impact from reduced fuel demand from the EU, US, and China as their fossil fuel exports represent more than 30 percent of their GDP; the CS3D regulation will increase costs for exporters in fossil fuel sectors due to new requirements for information gathering and reporting; Niger has the most exposed sector. (pp. 13-15, Figures 3-4)

- Developing countries’ energy-intensive exports will likely be affected by the EU’s CBAM and CS3D regulations, China’s ETS, and climate mitigation policies; CBAM will increase competitiveness and opportunities of exporters with lower carbon emissions but reduce competitiveness for exporters who cannot comply; the impact of CBAM on export competitiveness in countries with no carbon pricing will depend on the sector’s export orientation and its relative emission intensity; using an aggregate relative CBAM exposure index, developing nations like Zimbabwe, Ukraine, Georgia, and Mozambique could suffer significant competitiveness losses from CBAM while Albania, Colombia, Jordan, and Morocco could become more competitive; Mozambique and Ukraine have the greatest economic exposure to CBAM; CS3D will impact metal exports to the EU directly and indirectly, with Armenia’s metal value chain the most affected. (pp. 15-17, Figures 5-7)

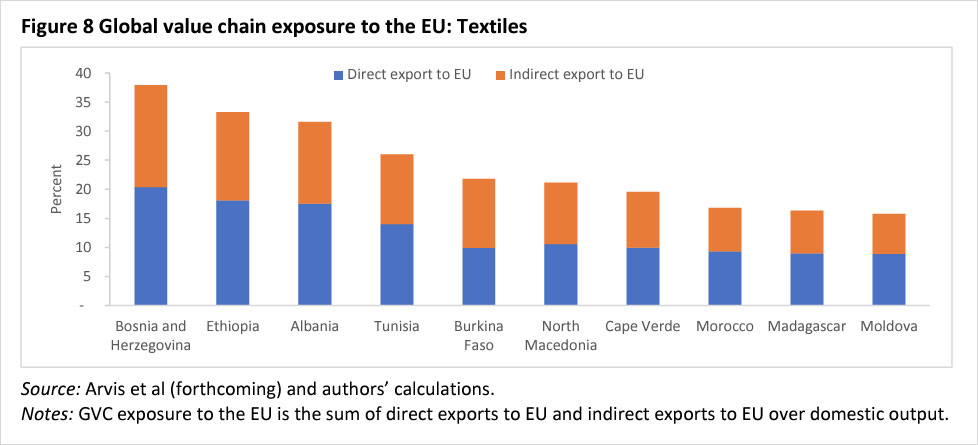

- EUDR will impact agricultural and forestry exports from developing countries by imposing strict tracking and environmental standards, increasing costs and decreasing exports to the EU; sectors heavily exposed to the EU will be most affected, particularly Sao Tome and Principe and Guinea-Bissau which send more than 95% of corresponding exports to the EU; CS3D will affect all industries with significant environmental footprints, including textiles; Bosnia and Herzegovina, Ethiopia, Albania, and Tunisia have the most exposure. (pp. 17-18, Figures 7-8)

- EU, US, and Chinese critical mineral policies will affect developing countries differently; Mongolia, North Macedonia, and Mozambique have the most exposed sectors as their exports are almost entirely directed to these economies; economic exposure is greatest in countries like Guinea and North Macedonia as a quarter of their GDP is from mining exports to these economies; CRMA will increase costs for critical minerals exports to the EU, but the EU’s demand from non-dominant mineral exporters will increase due to diversification requirements; in the medium to long-term, countries with abundant reserves will enter in or expand exports to the EU market as new mining operations arise; mineral reserve-rich developing countries may gain from the EU’s surging demand for critical minerals if they can scale-up production and improve competitiveness. (pp. 18-20, Figure 9, Tables 2-3)

- The IRA is expected to boost US demand for critical minerals, especially for green technologies, benefiting eligible exporters; established producers of raw and processed critical minerals for EV batteries with a US FTA are expected to see increased exports (Mexico), while those without an FTA (Brazil and China) could lose market access; in the medium term, countries with large reserves could negotiate an FTA or target non-battery related industries to enter the US market; China’s green energy transition will drive demand for critical minerals from developing countries with rising EV production increasing the need for battery materials; China’s ETS could lead to greater demand for components to upgrade gas- and coal-fired energy plants; recycling critical minerals can greatly influence trade with developing countries. (p. 20)

- EU, Chinese, and US policies are expected to boost demand for EVs and EV components from developing countries; countries with EV components sectors selling to these 3 markets stand to benefit the most, especially North Macedonia and Tunisia, whose EV component sales to these markets account for more than 5% of their GDP; for EV batteries, the DRC, Papua New Guinea, North Macedonia, and Bosnia and Herzegovina have the most exposed sectors, with more than 80% of their exports going to the 3 markets; the impact of the US IRA on battery sectors will change over time as US demand for imported EV batteries is expected to decline; US EV imports from developing countries may also decline; in contrast, the EU’s zero-emission regulation by 2035 may positively impact developing countries that export EVs as the rule’s requirements could increase demand beyond the EU’s domestic production capacity. (pp. 21-23, Figures 10-12)

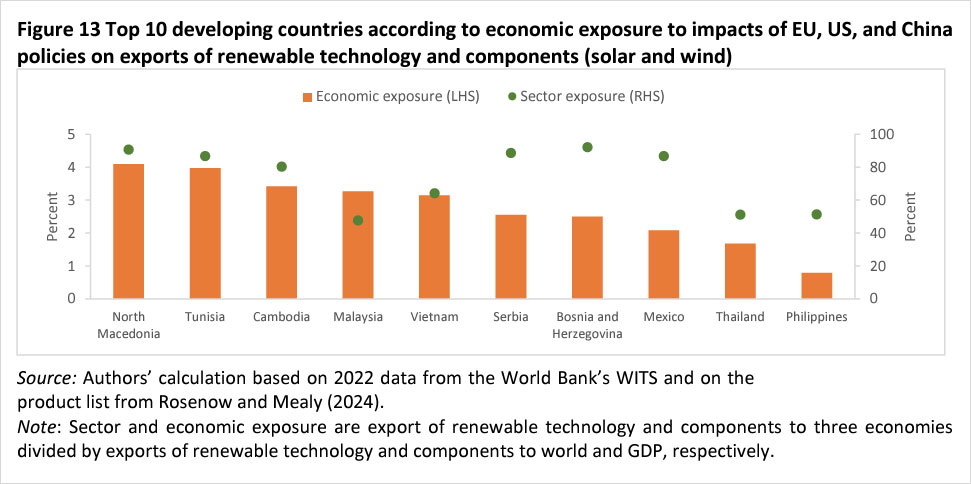

- EU, US, and China policies are likely to increase demand for renewable energy technologies and components; Bosnia and Herzegovina, North Macedonia, Serbia, Tunisia, and Cambodia are the most exposed with more than 80% of their exports going to the 3 markets, and renewable tech and components exports representing greater than 3-4% of their GDP. (p. 23, Figure 13)

- Current US and EU policies are expected to exert downward pressure on global oil prices and upward pressure on critical minerals prices over the medium to long-term by reducing demand for oil as renewable energy becomes more prevalent and as more minerals are needed for batteries and other green tech, combined with US unequal treatment for mineral sourcing; the US IRA will influence prices for products the IRA subsidizes; EU, US, and Chinese policies are also likely to increase developing countries’ access to green technologies: the Fit for 55 package underscores the importance of transferring technology to developing nations; the IRA could increase developing countries’ access to cost-effective green technologies after initial development in the US; China’s transfers will likely occur through BRI investments and R&D initiatives. (pp. 23-25, Figure 14)

Policy recommendations

- Measures can be taken to lessen the adverse effects of EU, US, and Chinese climate policies and capitalize on their benefits:

- Developing countries can boost export competitiveness in sustainable markets and support the development of green transition sectors by implementing climate mitigation policies (e.g., reducing emissions); promoting green goods and services, (e.g., reducing tariffs and non-tariff barriers on green tech); enhancing quality infrastructure and standards (e.g., improving certification and accreditation standards); supporting sectoral restructuring (e.g., helping workers transition to new jobs); improving the investment climate (e.g., reducing restrictions and enhancing trade facilitation). (p. 26)

- Developing countries with abundant critical raw materials can develop a comprehensive strategy to realize their potential for sustainable mineral extraction and processing; this can include development of mining-related infrastructure and clean energy sources to reduce mining’s reliance on fossil fuels; fostering upstream and downstream industries domestically while creating a supportive business environment can leverage EU, US, and Chinese demand to strengthen the economy and create jobs; exploring free trade agreements and long-term contracts to stabilize demand. (p. 26)

- The EU, US and China should avoid using protectionist tools in climate policies, like discriminatory subsidies and local content requirements, as these could spark a wave of copycat measures in other economies, slowing the green transition and hurting developing countries’ growth. (p. 27)

- The EU, US, and China should design green subsidies, carbon pricing, and regulations in a way that is neither more trade restrictive than necessary nor discriminatory and take in to account the impact on developing countries, helping them to adapt and reduce emissions more quickly. (p. 27)

- The EU, US, and China should harmonize carbon and environmental standards, regulations, and compliance procedures to reduce costs and ease the green transition; and to reduce supply risk for critical minerals, prioritize expanding global production rather than reshoring, segmentation, and thinning of markets. (p. 27)

- The international community can (i) assist in the execution of the recommendations for developing countries by providing financial aid and capacity building, engaging in collaborative projects, and sharing knowledge; (ii) develop a framework that reduces trade frictions stemming from diverse climate policies that includes a faster dispute settlement procedure responsive to the urgency of climate change, makes certain green subsidies non-actionable, and nudges countries toward greater climate policy alignment; and (iii) address emission intensity metrics and pricing, especially for goods with complex supply chains and cross-border issues; more research and analysis is needed to understand developing countries’ exposure and how to best to aid them. (pp. 27-29)

How to apply the insights

-

This section provides clear and concrete guidance for policy makers in both developing countries and in the US, EU, and China to be aware of when formulating climate policies, to ensure that their goals are not undermined by adverse impacts in developing countries, while also focusing developing countries on how best to leverage the opportunities provided by EU, US, and Chinese policies.

Conclusion

The Global Ripple Effects report provides food for thought for developing countries with sectors and economies exposed to or reliant on fossil fuels or green technologies and the inputs needed to produce them. The report also alerts the EU, US, and China to the potential negative impacts of their policies, in order to promote better policy construction, enabling these economies to achieve their climate goals for the benefit of the entire world.

Complementary reports and analysis

Hinrich Foundation

- Sustainable Trade Index 2024

- The geopolitics of climate change and cleantech

- Navigating the climate-trade nexus in Asia: A path to sustainability

- Are climate policies and trade policies on a collision course?

- Addressing the risk of carbon leakage: Assessing the EU’s carbon border adjustment mechanism

External Resources

- Trade and Climate Change – World Trade Organization

- Key Outcomes from COP29: Unpacking the New Global Climate Finance Goal and Beyond – World Resources Institute

- The return of industrial policies: Policy considerations in the current context – OECD

© The Hinrich Foundation. See our website Terms and conditions for our copyright and reprint policy. All statements of fact and the views, conclusions and recommendations expressed in this publication are the sole responsibility of the author(s).