Published 15 April 2025

Trump has issued a flurry of executive orders recently aiming to regain control of critical minerals. Yet, domestically, the US is struggling to reduce the byzantine US permitting process for mining. Internationally, Trump is trying to negotiate minerals deals with war-torn Ukraine and corrupt gangs in Congo and threatening to annex neighboring countries. To truly break China’s grip on the sector, Washington must work with allies.

It would be an understatement to say that the US struggles to develop mines. Analysis conducted by S&P Global found that the US has the second-longest lead time globally (29 years) for bringing mines from discovery to production. Despite supportive rhetoric on critical minerals and production credits under the Inflation Reduction Act (IRA), the Biden administration made little headway in revitalizing domestic mining. Only one – Ioneer’s Nevada lithium mine – was approved during President Biden’s term.

Balancing mining with biodiversity imperatives proved to be especially vexing. Other issues bedeviling US mining are deeply structural. One problem is that a huge array of often under-resourced, ponderous federal government agencies is involved in the permitting process. Unlike broadly comparable jurisdictions like Canada and Australia, the US lacks a dedicated mining ministry or coordinating agency.

Trump’s March Executive Order (EO) sought to cut through the regulatory knot. Its most contentious step was the changing of the mandate of the US International Development Finance Corporation (DFC), a federal development finance institution, to include domestic US mining projects. Subject to Congressional appropriations, this will notionally direct billions of dollars away from international development toward US mining projects.

Download Can Trump break China's critical minerals stranglehold? by Henry Storey:

Separately, even the most bullish advocates of American mining recognize that the US lacks the mineral resources to pursue autarky. The second iron in the fire is a slate of efforts to leverage raw American power to negotiate favorable bilateral minerals agreements, with Ukraine being the most prominent example. Exploiting Ukraine's mineral wealth – exaggerated by some accounts – will not be easy, however. Its only established rare earths deposit and 20% to 40% of its critical mineral reserves are under Russian occupation. Even the most audacious miners will be reluctant to invest in developing deposits amid an unresolved war.

Trump has also officially dispatched an envoy to engage in talks with the cobalt-rich Democratic Republic of the Congo (DRC), but the risks are rife: political leadership in the DRC is notoriously fickle and prone to charges of corruption. China retains huge influence in the country, potentially setting up unintended clashes should the US directly contest the market.

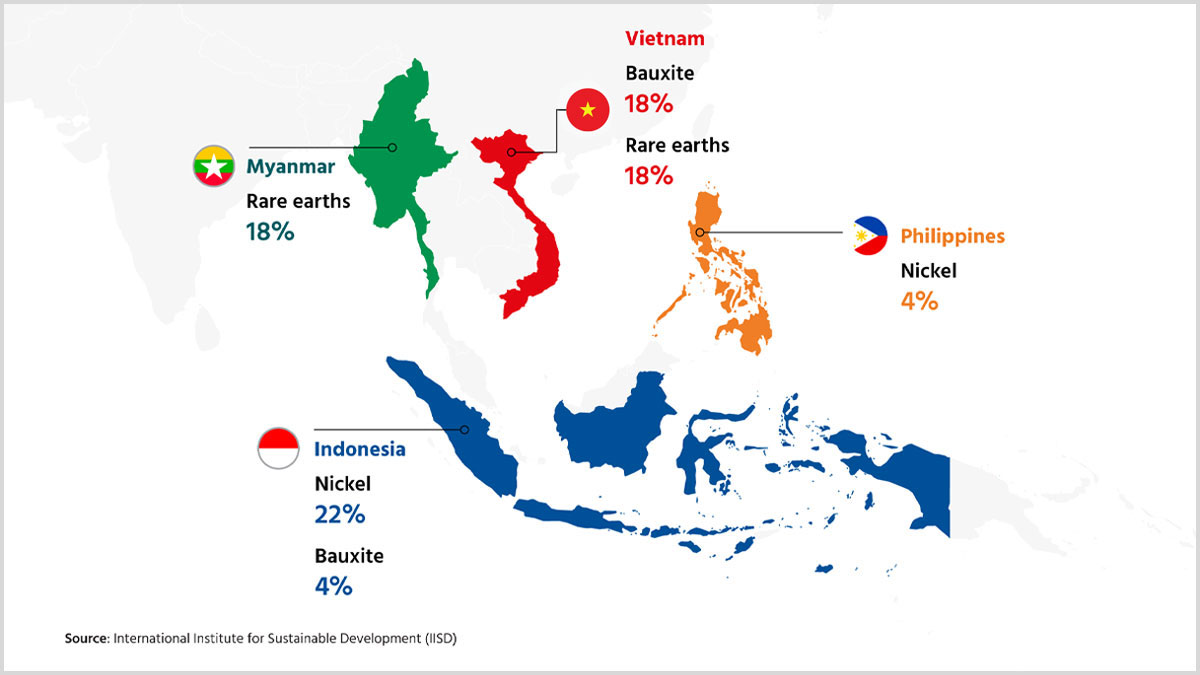

China’s dominance over rare earths and critical minerals is a product of both geology and prescient, well-funded industrial policy. Chinese companies control around 85% of the various stages of rare earths processing and 92% of the manufacturing of rare earth magnets. China also controls about 90% of global refining capacity for graphite and manganese, as well as approximately 80%, 70%, and 60%, for cobalt, nickel, and lithium, respectively. Since the Covid pandemic, the European Union, US, Japan, South Korea, Canada, and Australia have collectively committed billions of dollars in government support to the development of critical minerals mining and refining capabilities. These efforts have not been for nought. For example, lithium refineries have opened or are on track to open in all these locations.

Yet, subsidies and preferential loans are only part of the story. Western project proponents have accused Chinese companies of using their market dominance to intentionally depress prices, thereby destroying the business case for non-Chinese projects with higher costs and less state support. Prices of lithium, cobalt, and nickel dropped precipitously in 2023 and 2024 amid Chinese oversupply. In a recent comparison, The Economist noted that the operating margins, meaning the ratio of operating income to a company’s revenue, of Anglo-Australian giants BHP Group and Rio Tinto are around 20%-30%. Their largest Chinese competitors in copper, Zijin Mining and Jiangxi Copper, have operating margins of 11% and 2%, respectively.

It is at least plausible that Trump’s EO fusillade will help selected projects break through perennial regulatory logjams. Potential beneficiaries cited by mining experts include the Resolution copper project in Arizona, which alone could produce up to 25% of annual US copper demand. However, the operator Rio Tinto has faced a tough struggle to advance the project against environmental concerns and cultural heritage objections. It is not difficult to see how Trump’s push to rapidly truncate approval timelines could leave miners even more exposed to legal challenges. When all approvals and legal processes are finalized, Resolution is likely to still take around 10 years to build.

By far the most unorthodox element of Trump’s critical minerals strategy to date has been his fixation with annexing Greenland. The autonomous Danish territory has vast proven deposits of rare earths. So do parts of the deep sea and the moon. Here, the common underlying challenges are the costs of operating and developing the necessary infrastructure in fundamentally inhospitable environments. For all the hype, Greenland has just one producing mine. For now, any mines that are ultimately developed in Greenland will not be capable of competing with China without extensive government support.

Diversifying supply chains for rare earths and critical minerals is essential, but Trump’s current strategy is unlikely to significantly increase America's economic resilience. A much better course of action would be for Washington to work with allies and friendly nations – especially those with existing mining and refining industries – to catalyze the development of the finance and pricing mechanisms needed to compete with China.

© The Hinrich Foundation. See our website Terms and conditions for our copyright and reprint policy. All statements of fact and the views, conclusions and recommendations expressed in this publication are the sole responsibility of the author(s).

Author

Henry Storey

Henry Storey is a senior analyst at Dragoman, a Melbourne-based political risk consultancy. He is also a regular contributor of The Interpreter published by The Lowy Institute.

Have any feedback on this article?

Related Articles